If you’ve been waiting for mortgage rates to drop before buying your dream home along the Jersey Shore, there’s finally some good news. Rates have begun to ease — and experts predict there’s room for them to come down even more over the next year.

But how far will they go? And what’s driving this shift? To answer that, we need to look at one key indicator: the 10 year Treasury yield.

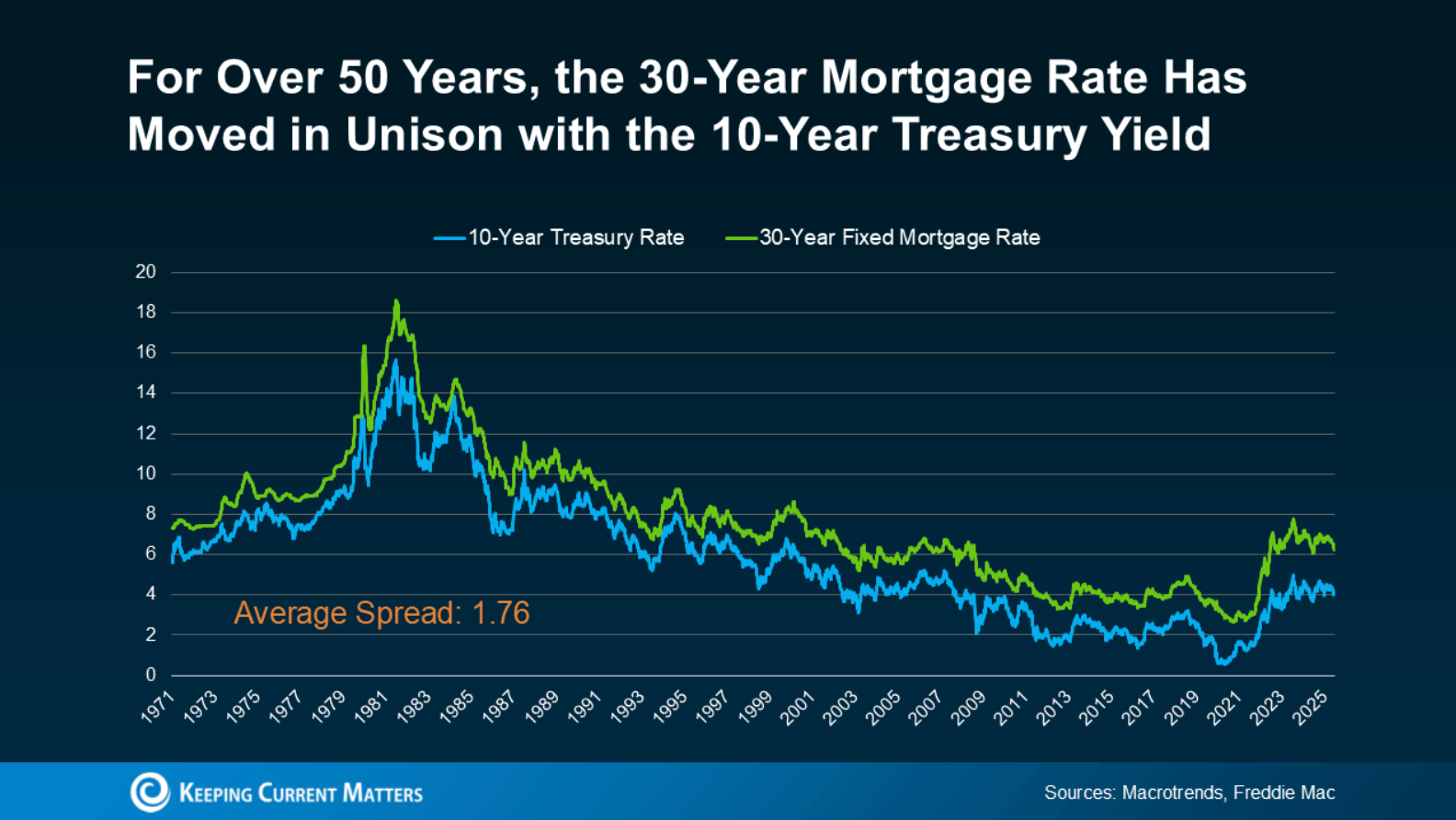

The Connection Between Mortgage Rates and the 10-Year Treasury Yield

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year Treasury yield — a benchmark for long-term interest rates.

When the Treasury yield rises, mortgage rates typically follow. And when it falls, mortgage rates tend to decline as well. Historically, there’s been a consistent “spread” between the two — averaging around 1.76 percentage points.

This relationship has long served as a reliable indicator for where mortgage rates are headed.

Why the Spread Matters — And Why It’s Shrinking

In recent years, the spread between the 10-year Treasury yield and mortgage rates has been wider than usual. That’s because uncertainty in the economy — from inflation concerns to global events — has kept investors cautious. A wider spread often signals “fear” in the market.

But now, we’re seeing that spread start to narrow again. As the economy steadies and the outlook becomes clearer, mortgage rates are slowly following suit.

As Redfin recently reported:

“A lower mortgage spread equals lower mortgage rates. If the spread continues to decline, mortgage rates could fall more than they already have.”

This is an encouraging sign for both buyers and sellers in the Bay Head, Mantoloking, and Point Pleasant real estate markets, where lower rates can bring more qualified buyers back into the market.

What Experts Predict for 2025 and Beyond

The 10 year Treasury yield itself is also forecasted to decline in the coming months. Combined with a narrowing spread, this creates two major forces pushing mortgage rates lower.

If these trends continue, we could see rates dip into the upper 5% range by late 2025 or early 2026.

For example, with today’s yield sitting around 4.09%, adding the typical spread of 1.76% would place mortgage rates near 5.85% — a meaningful shift for anyone considering a purchase or refinance.

Of course, fluctuations in the economy, job market, and inflation will continue to influence rates. But overall, the outlook points toward a gradual easing in mortgage rates — welcome news for homebuyers along the shore.

What This Means for You

For anyone looking to buy or invest in Jersey Shore real estate, this could be an ideal window to start planning. Lower mortgage rates mean increased purchasing power, and homes that once felt out of reach could soon fit your budget.

Whether you’re dreaming of a luxury waterfront property in Mantoloking, a Bay Head beach cottage, or a Point Pleasant family home, our team at Clayton & Clayton Realtors can help you navigate every step.

Bottom Line

The mortgage rate landscape is shifting — finally, in favor of buyers. If you want to stay informed about the latest rate changes and what they mean for your buying or selling plans, partner with a local expert who understands the Jersey Shore market inside and out.

At Clayton & Clayton, our family has specialized in Bay Head and Mantoloking real estate for over 95 years. We’ll help you make confident decisions in an ever-changing market.